Volatility interruption is one of the most important protective mechanisms in Xetra® trading on Frankfurter Wertpapierbörse (FWB®, the Frankfurt Stock Exchange). It ensures that exchange trading runs smoothly even in extreme market conditions.

February 24, 2022 was a turbulent day for financial markets all over the world. The start of the war in Ukraine was the cause of a highly volatile mood on the stock markets. Prices slumped in the double-digit percentage range just about everywhere but recovered to some extent during the day. That day, the stock exchange infrastructure came under pressure, the likes of which it had not experienced since the start of the coronavirus pandemic. However, thanks to established protective mechanisms, exchange trading continued to function smoothly.

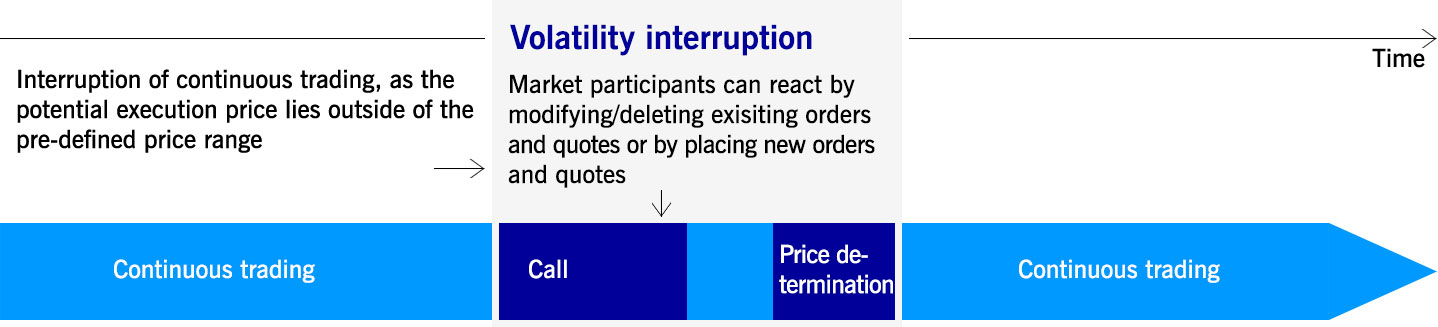

The volatility interruption, or “vola” for short, made an important contribution that day. If the price of a security starts to swing too wildly, trading is switched automatically from continuous trading to auction for at least two minutes. This decelerates trading, gives market participants time to get their bearings and prevents the market from taking off unchecked in one direction.

Another important factor is that trading in the affected security is not suspended when a volatility interruption is triggered. Suspension generally results in even greater uncertainty amongst market participants and further increases volatility. In the auction phase, which replaces continuous trading, market participants can continue entering, changing and deleting their orders. Of course, during the auction, orders are not automatically executed immediately, but collected until the end of the auction phase. Market participants continue to see an indicative auction price, i.e. the price that would be struck if the auction were to end at that given moment. That way, the consequences of the situation remain calculable for all trading participants.

Advantages of the volatility interruption at a glance

- It prevents large price swings regardless of the direction the market is moving – swings caused e.g. by incorrect order entry, illiquid market conditions or the entry of unlimited orders with too high transaction volumes.

- This gives market participants an opportunity to adjust their view of the market by looking at the overall situation, taking other markets into account and checking their own order situation.

- It gives all participants the opportunity to analyse the situation calmly during an extremely hectic market phase.

- It bundles market liquidity: a price based on orders from many market participants is considerably more robust and indicative than a single price based on only two orders in a fast-moving market.

- In case of very large price jumps, Deutsche Börse's market supervision is also given the opportunity to check the situation - for example, order book, news situation or reasons for the disruption.

Individual price corridors act as triggers

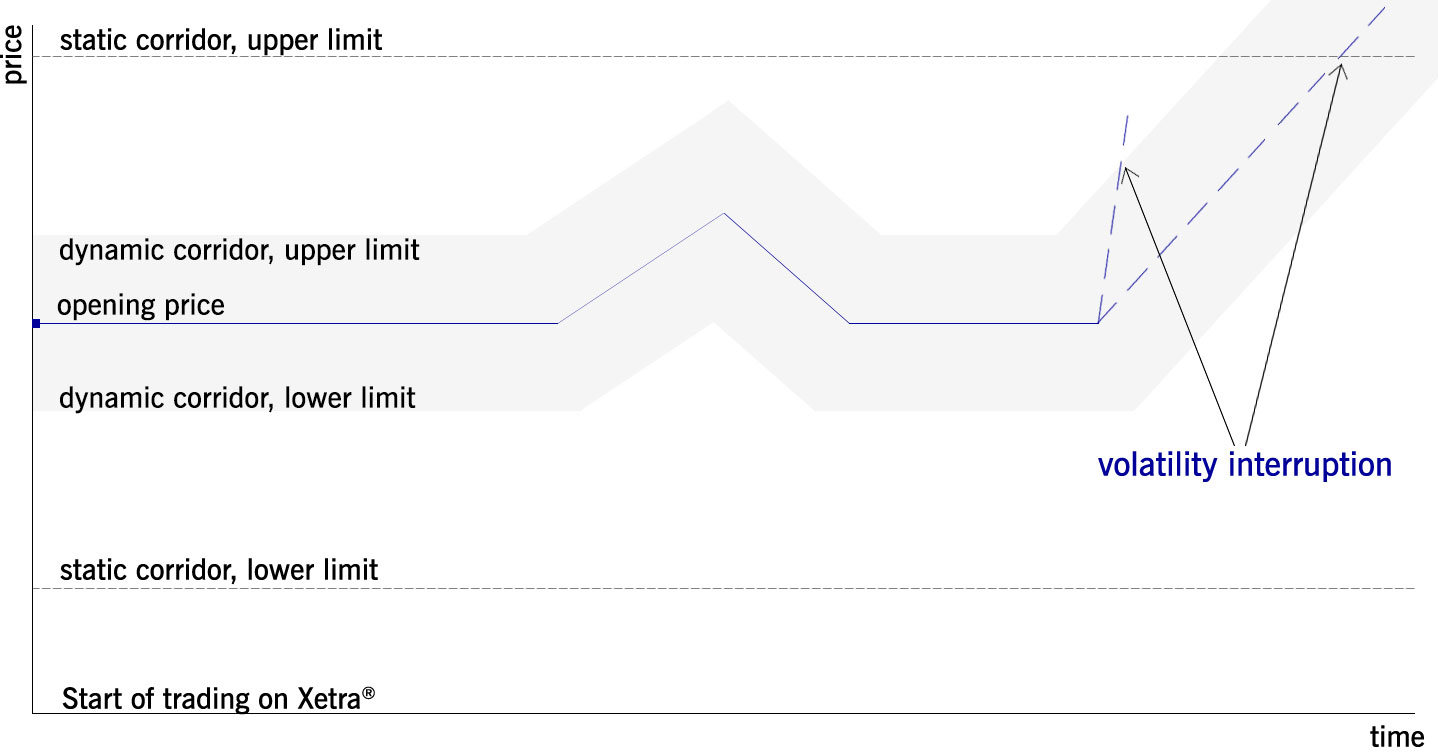

So, what triggers a volatility interruption? Every security in Xetra trading has two individual price corridors, a static one and a dynamic one. These corridors develop during continuous trading along with the price of the security. The static corridor is based around the opening price in the morning and is relatively wide. The dynamic corridor is narrower and brackets the last price determined. The volatility interruption is triggered if the price lies outside one of these corridors at the next pricing. Trading then switches from continuous trading to an auction with a duration of at least two minutes. The auction ends at a random point in time to avoid price manipulation. The concrete course of this auction is determined by the volatility interruption model that is used, whereby a distinction is made between the Single Volatility Interruption Model and the Automated Corridor Expansion (ACE) Volatility Interruption Model.

What happens after the volatility interruption has been triggered?

In the Single Volatility Interruption Model, the price is determined within a single, previously defined price corridor. If the price determined at the end of the volatility interruption is within this price corridor, the auction can be terminated and a switch back to continuous trading can be made.

The ACE Volatility Interruption Model, on the other hand, uses several subsequently expanding price corridors. Here, after the expiration of a minimum duration for each individual price corridor, the possibility of a price determination within the respective corridor is checked. If the price determined is within the price corridor after expiry of this minimum duration, the auction can be terminated. Otherwise, the auction is extended, and the check is performed again in the subsequent price corridor after the minimum duration has expired.

If, after passing through all defined price corridors, the determined price continues to lie outside the then valid price corridor, the system switches to an extended volatility interruption. In this case, the market supervision of Deutsche Börse, which continuously monitors the process, intervenes and manually terminates the volatility interruption while considering the overall market situation and auction process. As soon as the market supervision concludes that the auction order book leads to a robust new price level, the auction price is established, and continuous trading is resumed.

Additional protective mechanisms

There are protective mechanisms such as the volatility interruption along the entire trading process chain. For instance, when an order is entered, the trading system checks it for plausibility in order to, for example, avoid the limit and the volume being mixed up during input. In addition, a variable “curbing mechanism” ensures that the maximum number of orders per second is technically limited, so the entire system is not slowed down by individual participants. Then, in order execution, the independent Trading Surveillance Office, or HüSt for short, makes certain that a fair price is determined for every investor in accordance with exchange rules. And in post-trading, Eurex Clearing, Deutsche Börse Group’s clearing house, ensures that risks are minimized through real-time management and that the securities are actually delivered and paid for.