Börsengeschichte(n)_EN

Exchange history and stories There have been financial markets for as long as people have been trading with one another

The German term “Börse”, meaning “exchange”, comes from the 15th century: in the Belgian city of Bruges, it described a regular gathering of rich Italian merchants at Ter Buerse square, a regular rest stop on their way to the cloth fairs in the Netherlands. This marketplace was named after the patrician family van der Beurse, who lived there (Lat. bursa = purse).

The Frankfurt fair on the Römerberg

Copyright: Historisches Museum Frankfurt am Main

As there was no single currency back then and the countries had fragmented into a number of small economic areas, each with their own monetary system, a wide variety of coins were used to pay at the fairs. The copious means of payment and free exchange rates enabled profiteering and fraud.

In 1585, for example, merchants met in Frankfurt am Main, a major fair venue, to counter this proliferation of coins by setting uniform exchange rates. Today, this event is seen as marking the birth of the Frankfurt Stock Exchange. From then on, uniform and binding prices were regularly updated at fair time.

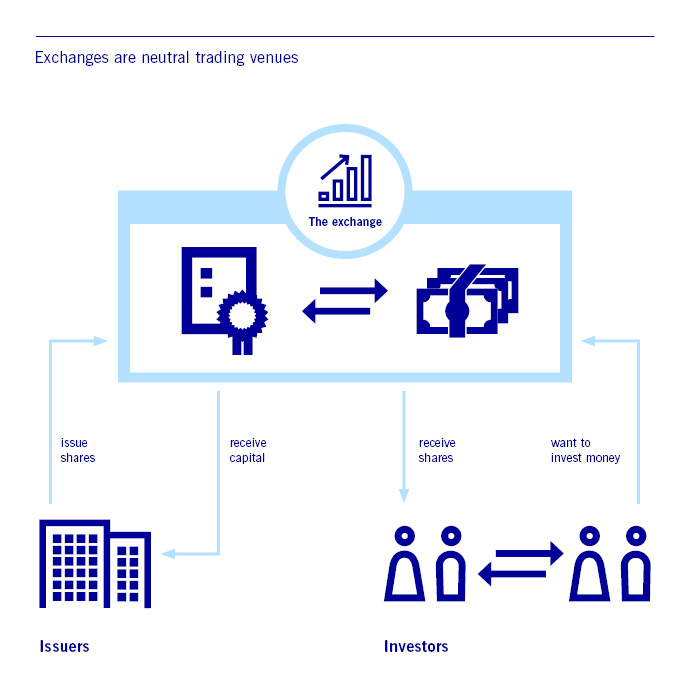

Who is who on the exchange?

{kind=link}

Issuers

Issuers are companies that need funds to finance their investments. By listing on an exchange, companies both large and medium-sized, national and international, can issue securities on the market, thereby making them tradeable and raising capital for growth or necessary investments. Securities are not only issued by companies but also by municipalities and states.

Investors (buyers and sellers)

Investors purchase securities or other financial instruments and then trade them on the exchange in order to invest their money, hedge against future losses or pursue particular corporate strategies (e.g. mergers) – or they sell their securities again if they need funds themselves. This enables investors to share in issuers’ growth and also to promote it by investing capital.

Exchanges

In Germany, exchanges have a public function: they are supposed to ensure orderly trading, transparency and the equal treatment of market participants. They ensure that trading is conducted in an orderly manner through their trading platforms, most of which are now fully automated, and by putting in place appropriate rules and regulations.

They provide the infrastructure (i.e. the “marketplace”) and bring together buyers and sellers of securities. They do not buy or sell themselves.

Exchanges do not influence the discovery or performance of securities prices. These are determined solely by agreement between buyers and sellers. The more active trading is, the more liquid the market, i.e. the more likely it is that a buyer will find a seller and vice versa.

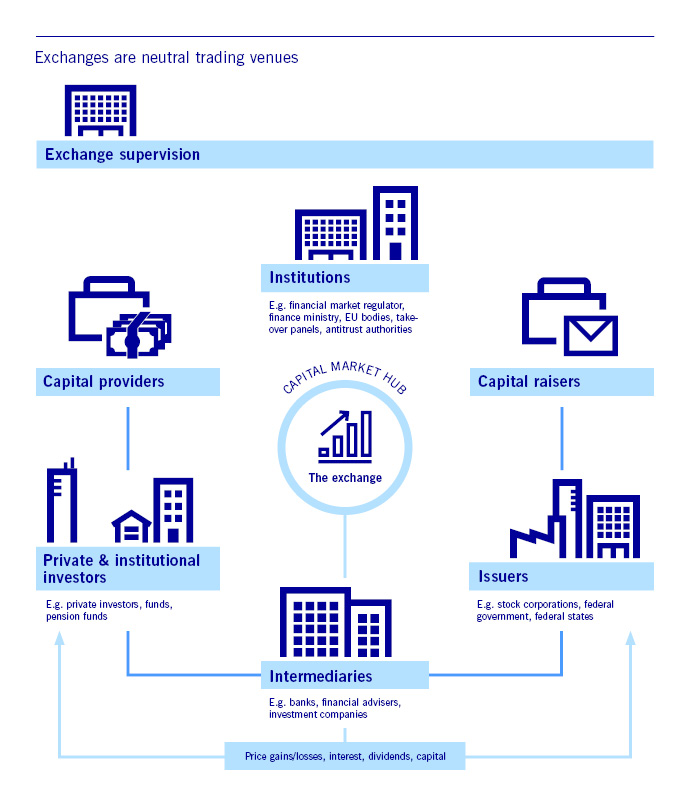

Exchange supervision

As the executive body, the management of an exchange is entrusted with carrying out the public administration transferred to that exchange. It ensures that rules and regulations are observed. The exchange supervisory authorities in Germany are the ministries of economic affairs or finance and the senate administrations of the federal states. They supervise the exchanges in accordance with the Börsengesetz (BörsG, German Stock Exchange Act) and ensure orderly exchange trading.

The Handelsüberwachungsstelle (HÜSt, German Trading Surveillance Office) is an independent exchange body responsible for market supervision locally. It monitors the price quotations and trading at the exchange both on the exchange floor and via fully electronic trading systems. The HÜSt investigates irregularities and notifies the relevant exchange supervisory authorities and management teams of the findings of its investigations.

Who may trade on the exchange?

Generally, anyone who wishes to trade on the exchange may do so. All they have to do is place a buy order for a single share.

Private individuals cannot go onto a securities exchange trading floor themselves and buy and sell shares there. They have to issue, or “place”, buy and sell orders through a bank that is admitted to trading on the exchange.

For this, investors need a securities account at a bank. A number of banks and brokers (institutional traders) are admitted to trading on the exchanges. However, they can also forward their clients’ securities orders to the exchange through a specialist securities trading bank.

Deutsche Börse Group

Headquartered in Frankfurt/Main, Deutsche Börse Group is one of the largest exchange organisations worldwide. It operates markets that provide integrity, transparency and security for investors wishing to invest capital and for issuers wishing to raise capital. On these markets, institutional traders buy and sell shares, derivatives and other financial instruments in accordance with clear rules and under strict supervision.

Deutsche Börse Group is now more than just a trading venue or exchange – it is a provider of financial market infrastructure. Its products and services span the entire finance value chain – its business areas range from pre-IPO services and the admission of securities, through trading, clearing, settlement and custody of securities and other financial instruments to collateral management. It also offers IT services, indices and market data worldwide.